Did I say mandatory? I meant optional! You’re “free” to die in a cardboard box under a freeway as a market capitalist scarecrow warning to the other ants so they keep showing up to make us more!

I think dividends in a tax-exempt accounts, like a traditional IRA, are only not taxed if you reinvest the dividend or just leave it in your brokerage account. If you move money from your IRA account to, say, your checking account, that’s when you pay taxes (and there are generally fees for moving money out of tax exempt accounts without meeting certain conditions, like being of retirement age).

{kind=link}

{kind=link}

I think dividends in a tax-exempt accounts, like a traditional IRA, are only not taxed if you reinvest the dividend or just leave it in your brokerage account.

Right. Although, with a ROTH IRA, you pay taxes before you put the money in. Then you earn tax free even after you take it out. That makes it the preferable vehicle for long-term savings (you should expect your initial investment to double every 10 years, assuming a 7% ROI which is fairly modest - so over 30-40 years you’re saving 8x on the eventual withdrawal).

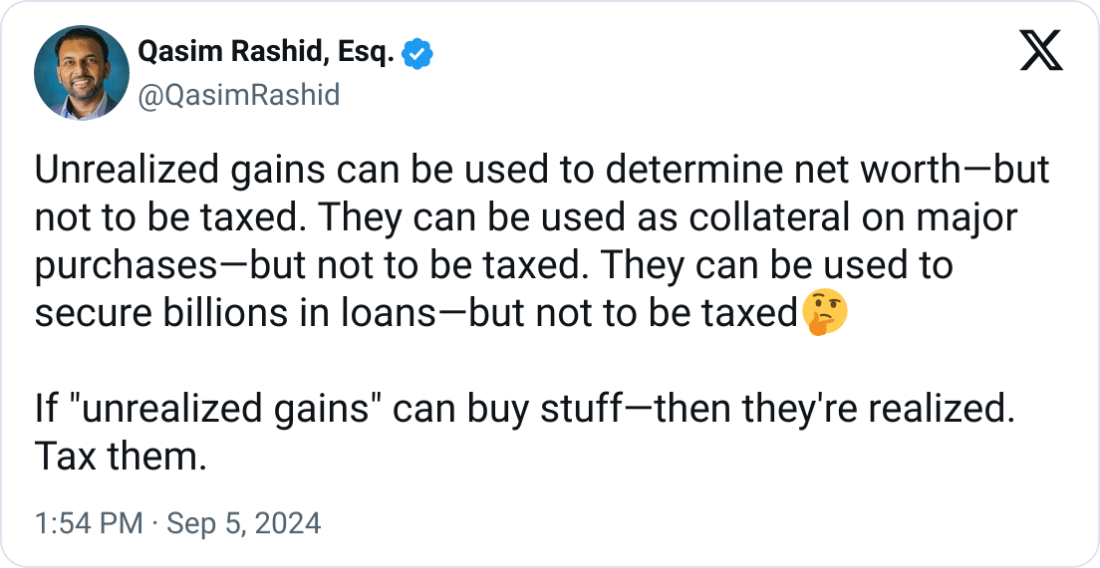

But this isn’t just limited to IRAs. Using investment funds, you can pull the same trick. Buy the fund, then allow the broker to shuffle the investments within the fund as they please. You only “earn” the money when you exit the fund, in the same way you only “earn” your retirement when you withdraw from your IRA.

Savings accounts and trusts can then be structured to be inheritable tax-free, with your heirs having access to withdraw from the fund without ever actually owning the money (and thus needing to pay taxes on the inheritance). And to make it even more squirrelly, you can borrow against these funds, which allows you to make large purchases without ever actually spending any money. This maneuver, plus a cagey use of declared loses, means you can avoid paying any tax on any investment income virtually indefinitely.

Thanks for expanding on the finer points! With inheritance, they also reset the cost-basis when the owner dies, which means that all the capital gains accumulated over the time that the deceased had ownership is never taxed. Like, if I bought stock for $10, die when it’s worth $100, my sister inherits it, and then sells it for $110 a while later, she only pays capital gains on $10 – not $100.

I don’t think people fully realize how dramatically our tax code rewards capital, at the expense of labor, not just in the broad-strokes (like the tax rate for capital gains vs the rates for income tax brakets) but also in these little details that are easy to overlook. So thanks for the discussion!

I largely agree with all the points made here however I think the overall message is a bit misleading. I would disagree that Roth investments are the preferred for long term investments. You aren’t accounting for the opportunity cost of the taxes paid in the initial investment year. Those taxes, while small compared to what you will withdraw tax free are also losing out on 8x-ing themselves (as you would have invested that amount in a traditional tax advantaged account).

What this means is Roth is the preferable savings method if you are in a lower marginal tax rate than you expect to be in retirement. However traditional is better if you are in a higher marginal rate than you expect to be in retirement. If the marginal tax rate was the same when you invest and retire then the difference between Roth and traditional would be nil.

You aren’t accounting for the opportunity cost of the taxes paid in the initial investment year.

If you’re maxing out your contributions, it won’t matter, except in so far as what you can earn on taxed income outside of the IRA account. That’s going to be marginal relative to the contribution. And the compound returns inside the IRA make it meaningless.

What this means is Roth is the preferable savings method if you are in a lower marginal tax rate than you expect to be in retirement.

Unless you’re going straight into a white shoe law firm or extraordinary paying tech job after you graduate, that’s pretty much everyone. But even folks going into Fortune 500 companies typically start in the $60-80k/year range and climb up from there.

If the marginal tax rate was the same when you invest and retire then the difference between Roth and traditional would be nil.

The amount of money you have in the fund is going to be much larger.

Say I invest $5000/year up front and get a 10% return for 40 years. I’m looking at putting in $200,000 over that time and taking out $2.2M.

Assuming the tax rate is 25% for each of those years, I paid $50k in taxes to invest that initial $200k. But I get the $2.2M back tax-free.

If I put the $200k in tax-deferred, I have to pay $550k to get my balance out again.

Now, we can argue that I could put the $400/year in deferred taxes into a taxable savings account. And maybe we get clever by shielding that investment from taxation annually because we just shove it all in Microsoft or Berkshire B and let it ride. That nets me another $177k over 40 years, assuming the same rate of return (for which I’m still on the hook at 15% long term gains rate - so really only $150k).

The ROTH is $350k better. That’s the whole reason the fund exists. It’s another accounting gimmick to give wealthy people a stealth tax cut. Only suckers put their money in Trad IRAs.

There is a big maybe on whether Roth is better than traditional IRA/401k.

My kids are at the age where they are making those bets now. So I made a hugely complicated forecasting tool to forecast which would be better.

I think it really comes down to your view on future tax rates.

Your mileage may vary.

I think it really comes down to your view on future tax rates.

Unless you’re banking on a 0% tax, the ROTH is hard to beat. Compound that by the Traditional IRA being taxed at the normal rate rather than the capital gains rate, and there’s very little reason to use it unless you’re really bullish on tax cuts in the long term.